Q1 by the numbers

Articles

The Q1 2026 multifamily market by the numbers

May 1, 2026

Market Updates

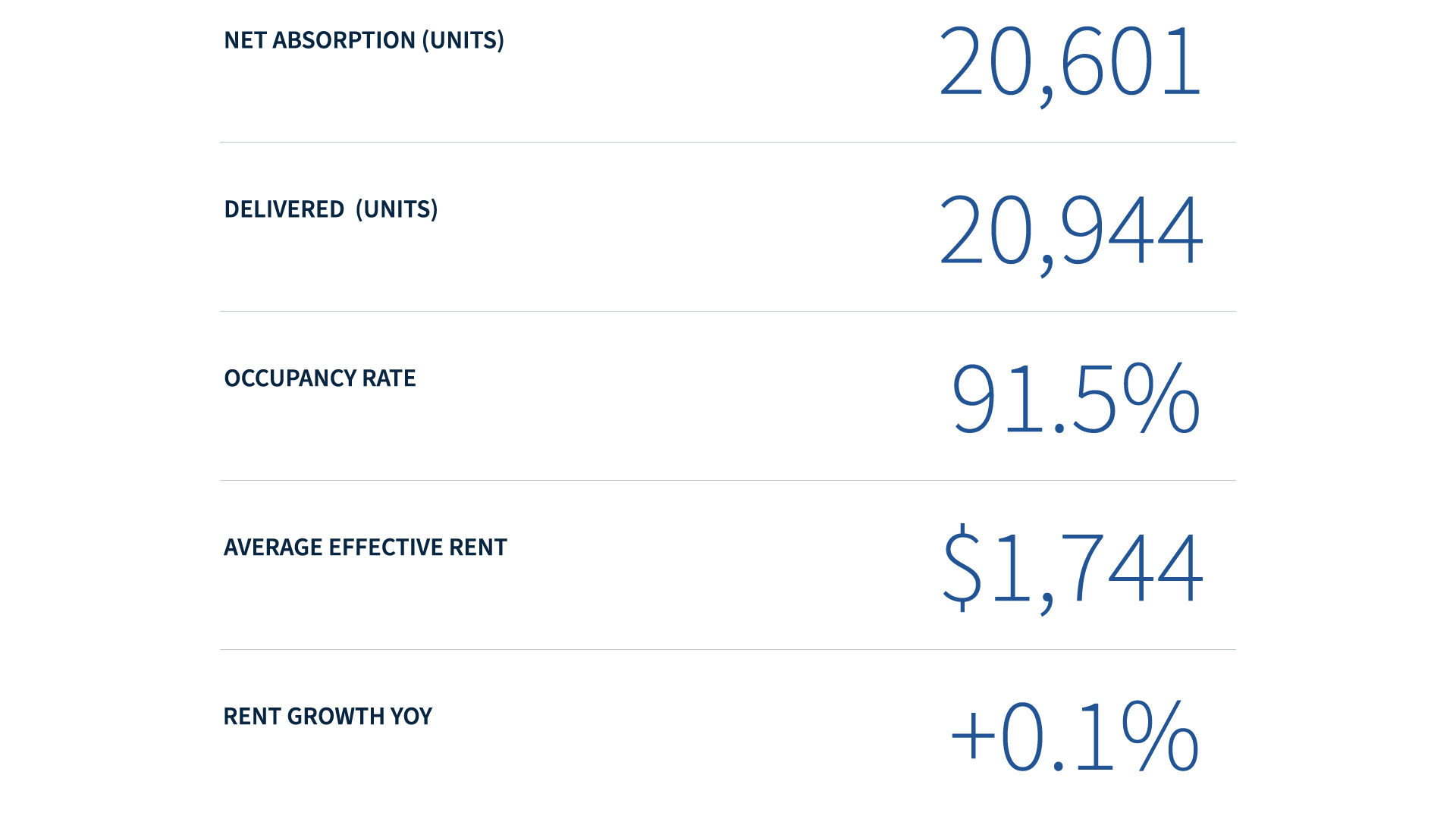

Multifamily deliveries marginally exceeded absorption in the first quarter of 2026, a trend expected to persist throughout the rest of 2026. As new construction activity tapers off and demand picks up, especially in Sunbelt markets like Dallas and Atlanta,1 absorption could again exceed deliveries and cause U.S. apartment rents to grow.

This quarter saw gradual progress in that direction, thanks in part to a moderating pace of development. Nationwide multifamily construction starts fell to 51,741 units in Q1 2026, down from over 74,000 units in the fourth quarter of last year and nearly 92,000 units in Q3 2025.1 Completions, while elevated from last month, similarly fell over 15% as compared to January 2025.1

A persisting (though moderating) supply-and-demand imbalance is causing temporary occupancy and rent growth headwinds. Vacancy currently sits at 8.5%, while annualized rent growth is essentially flat.1

However, CoStar estimates that vacancy is broadly plateauing—and even declining for attainable properties—thanks to heightening lease-up activity.

This improvement in leasing activity is driven in part by the fact that renting makes financial sense. As of March 2026, renting is cheaper than owning in every one of the top 50 metropolitan areas in the United States.2 In Sunbelt cities like Austin, Phoenix, or Dallas, the monthly cost of homeownership exceeds the cost of rent by over $1,100 per month.2 Even markets with narrower price gaps between renting and owning, such as Orlando, see renters save roughly $300 per month compared to homebuyers.2

For this reason, 3 in 5 renters surveyed by Zillow say they plan to continue renting by choice in 2026—even if they have the means to buy a home.3 Even if mortgage rates fell and homeownership became more affordable, just 37% of polled renters say they would be interested in buying, down from 45% in 2024.3 This suggests that financial considerations are only part of the reason why Americans choose to rent, with perks like greater amenities, more flexibility, and a maintenance-free lifestyle also pulling residents towards renting and away from buying.

As a result of this trend, CoStar expects the quarterly absorption to exceed deliveries throughout the remainder of 2026. If that materializes, rents could accelerate through the end of 2026, with forecasts suggesting an uptick of 0.6% for the year.1

The first quarter of 2026 has reinforced our view that the U.S. multifamily market is approaching a meaningful inflection point, though the path has grown more nuanced than the trajectory we outlined last quarter. Capital markets liquidity has returned, total deals sold were up 9% year-over-year, resembling 2019 levels of activity, and the construction pipeline is contracting at a pace that sets up favorable supply dynamics in 2027 and beyond.4 At the same time, renewed interest rate volatility, geopolitical risk, and a cooler labor market have replaced the unidirectional optimism of late 2025 with a more balanced near-term outlook.

We continue to believe that 2026 marks the early innings of a new cap rate compression cycle, though the timing and magnitude of debt cost relief may extend further than we previously anticipated. Treasury yields drifting upward and the Fed's pause on additional rate cuts suggest that financing costs may grind lower rather than fall sharply over the coming 12 months. Even so, the fundamental setup, a 48% contraction in the construction pipeline, deliveries projected to fall to a 12-year low in 2026, and stabilized cap rates already firming for high-quality assets, supports our thesis of meaningful asset value appreciation as occupancy rebuilds and NOI improves.

DLP continues to expect a return to positive, normalized rent growth as the current supply wave is absorbed. Absorption is projected to begin outperforming deliveries in the second half of 2026, with rent growth accelerating by year-end and improving further into 2027 as stabilized vacancy slowly recedes. We anticipate NOI improvements driven by both revenue gains, through rent growth and reduced concessions, and continued moderation in operating expense inflation, particularly in payroll, maintenance, and turnover costs.

Overall, DLP Capital believes that disciplined execution of our proven investment strategies and patient capital deployed through this rebalancing period will continue to drive performance across the Funds and support our annualized net return targets.

Our website uses cookies to enhance your experience, analyze website traffic, and deliver content tailored to your interests. By clicking "Accept", you consent to our use of cookies.