Diversify with private credit and equity real estate investment funds that make non-concessionary impact investments to expand access for America’s working families to affordable, safe communities.

Senior Secured Mortgage Fund that makes private credit investments to experienced real estate sponsors. Targets monthly passive income and annual returns of up to 10% for accredited investors.

Private Real Estate Investment Fund that invests in income-producing, attainable rental communities. Targets monthly passive income and annual returns of up to 12% for accredited investors.

Private Preferred Credit Fund that provides mezzanine loans and other subordinate financing to developers focused on attainable rental housing. Targets monthly passive income and annual returns of up to 11% for accredited investors.

Private Real Estate Investment Fund that invests in all stages of development to build, improve, and manage attainable rental housing. Targets quarterly passive income and annual returns of up to 14% for accredited investors.

Private Real Estate Investment Fund focused on manufactured housing and RV-zoned communities, including vacation rental resorts and hospitality-integrated developments. Invests in the sale of manufactured homes and park models paired with land-lease structures. Targets long-term equity growth with a preferred annual return of approximately 10% for accredited investors.

Structured Private Note Offering providing priority credit exposure to DLP-managed real estate assets through secured Series A Notes. Designed to deliver fixed, predictable income with an 8% annual interest rate, monthly reporting, and a 5-year term for disciplined accredited investors.

See how DLP Capital’s lending fuels real estate projects that transform communities. These stories highlight the creativity, determination, and results of the talented sponsors we work with.

Explore a selection of our recent transactions across lending, acquisitions, and investments — demonstrating our commitment to delivering momentum, certainty, and impact for real estate projects nationwide.

Our core value of Driven for Greatness is about adopting a growth mindset and consistently seeking out opportunities to learn. The Twenty is our way of helping you do just that, named after the core value that sets the tone for all we do: the Twenty-Mile March. Learn from our latest webinars, articles, podcast episodes, and more.

In his blog, Founder and CEO Don Wenner shares insights from the lessons he’s learned as a faith-driven CEO who has grown DLP Capital to be an Inc. 5000 Fastest-Growing Company for 13 consecutive years at just 40 years old. Learn not just from his own experiences as an entrepreneur, father, and husband, but the most important lessons he has learned from friends and mentors like John C. Maxwell, Lloyd Reeb and others.

From impact investing to building an extraordinary organization while being equally focused on an extraordinary family, Don Wenner’s Elite Impact Podcast covers it all. Learn valuable insights and hear incredible stories of leadership, impact, and more from Don and his guests.

Experience DLP Capital events anytime. Watch keynotes, panel discussions, and training sessions featuring industry leaders and experts driving innovation and impact.

Access DLP Capital’s complete webinar library, featuring quarterly fund updates, educational sessions, and special presentations designed to keep investors informed and inspired.

Read the latest DLP Capital quarterly report for the most recent performance of DLP Capital-sponsored funds, updates on current investments within the funds, stories of our impact in action, company insights, and more.

CEO Don Wenner has built a life—and a company—dedicated to transforming lives through access to safe and attainable housing. Today, DLP Capital is creating solutions to the affordable housing crisis, redefining community, and helping investors discover success with significance.

DLP Capital’s purpose-driven, non-concessionary impact investments create housing, jobs, connection, and opportunity for families across America. Discover more about how DLP invests with purpose.

Meet the visionary leaders committed to executing DLP’s vision of transforming the lives of both residents and investors through the building of Thriving Communities.

Stay inspired by the latest updates from DLP Capital. Explore how we’re driving meaningful change, earning recognition, and celebrating milestones as we continue building thriving communities across America.

At DLP Capital, work is more than a job—it’s a mission. Join a team dedicated to solving America’s housing crisis, building thriving communities, and creating opportunities for families across the country.

Our mission starts with connection. Reach out to our team or visit one of our locations to learn more about how DLP Capital is creating impact where it matters most.

Real Estate vs. Stock Market Returns: Which is Right for You?

10–20% declines are common in the stock market. How does real estate compare?

May 17, 2025

Market Updates

As an investor, you’ve likely felt the impact of recent market turbulence.

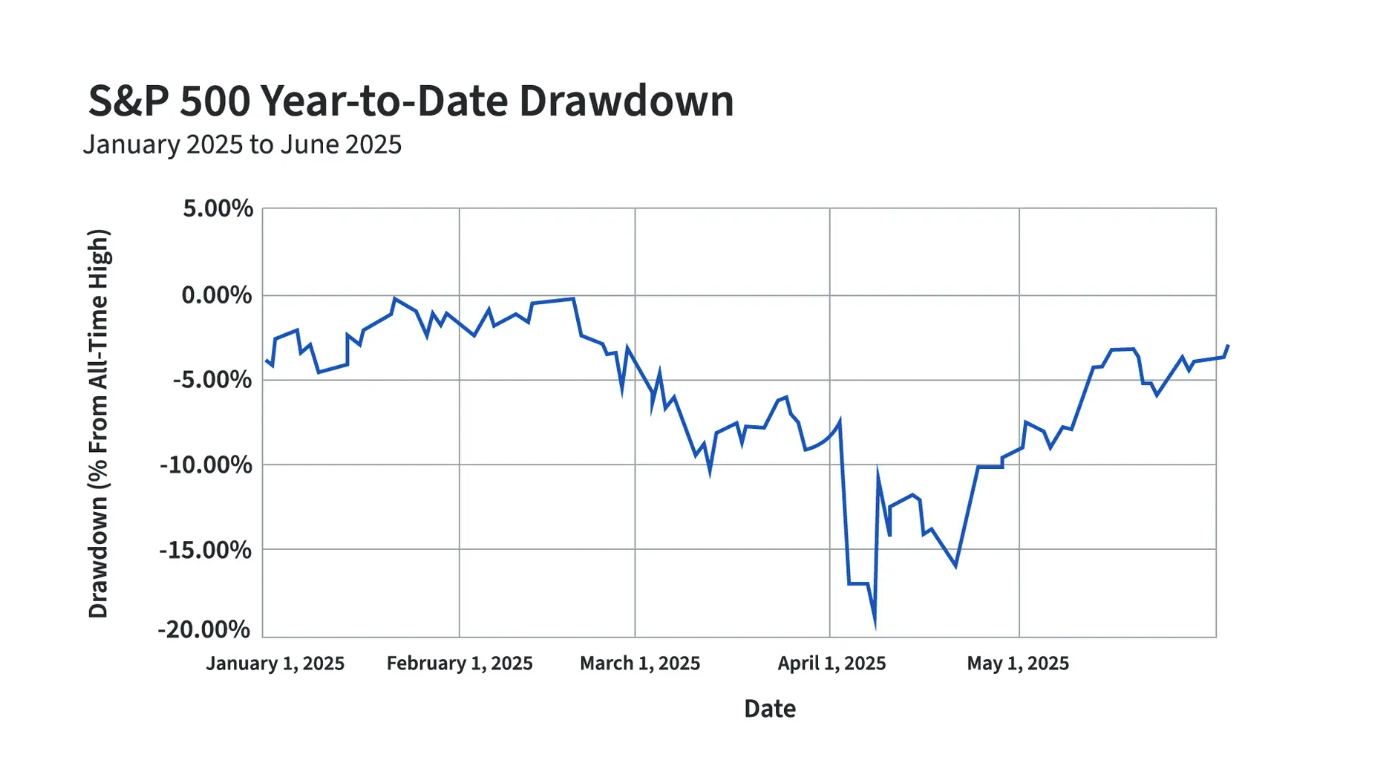

In April 2025, equities lurched towards a technical bear market—defined as a peak-to-trough decline of 20% or more—as business policy uncertainty and unfavorable tariff news cratered investor sentiment.

The S&P 500, the most widely-benchmarked index in the United States and around the world, plunged 18.9% on a peak-to-trough closing basis in the roughly two months between Tuesday, February 19 and Tuesday, April 8, barely a percentage point shy of the bear market threshold.1

Public markets have since staged a rapid rebound. Thanks in part to a 90-day stay on a 145% tariff rate with China, the S&P 500 opened the month of June 2025 less than 4% from a new all-time high.2

But stock market investors may not be out of the woods yet. Absent further action, tariffs could resume on July 8,2 meaning that investors may potentially have to brace for additional volatility in the coming months.

Besides, not all market recoveries are that rapid, at least historically speaking. It's common for stock market investors to wait years—and sometimes even a decade or more—to regain losses after a significant downturn. Consider recent history:

2022–2023: After a 25% decline between January and October 2022, the S&P 500 didn’t regain an all-time high until January 2024.3 That meant investors spent two full years (2022 and 2023) in a drawdown.

2000s: Even more dramatically, the S&P 500 returned essentially nothing in the decade-plus between 2000 and 2013, thanks to the biting “dot-com” implosion of 2000–2003 and the even sharper Global Financial Crisis of 2007–2009.3

Experiencing these prolonged drawdowns can be stressful. Beyond the emotional toll, spending years simply recovering losses means your capital isn't actively growing towards your long-term goals. It highlights a key challenge in public markets: significant risk doesn't always guarantee commensurate returns, and dramatic declines can be a frequent visitor.

So, what alternatives can you consider if you want to diversify away from public market volatility without sacrificing return potential?

So, what alternatives can you consider if you want to diversify away from public market volatility without sacrificing return potential?

Private real estate: a promising alternative?

For investors seeking to diversify away from the daily drama of public markets, private real estate could be a potentially compelling alternative.

Historically, private real estate has demonstrated lower volatility compared to the stock market.3 That’s because the valuations of real estate and the private funds that own them tend to be more stable and change more slowly. This stands in sharp contrast to publicly-traded assets, which tend to fluctuate dramatically based on news, sentiment, or trading algorithms.

Private real estate could be especially beneficial for portfolio diversification, too. According to Ares Wealth Management, “private real estate had a 0.04 correlation to the S&P 500 Index over the past 20 years, and a negative correlation of 0.28 over the past 10 years.”4 In short, this means that private real estate may perform well even in a year where the stock market is struggling, which in turn suggests that allocating part of your portfolio to private real estate could help cushion the overall impact on your wealth.

A closer look at multifamily

Within the broader landscape of private real estate, multifamily properties could offer specific advantages that may be particularly attractive. Specifically, investing in private multifamily real estate funds—which pool capital and invest in large baskets of loans or multifamily properties—could offer a different risk-reward profile and potentially more consistent return patterns.

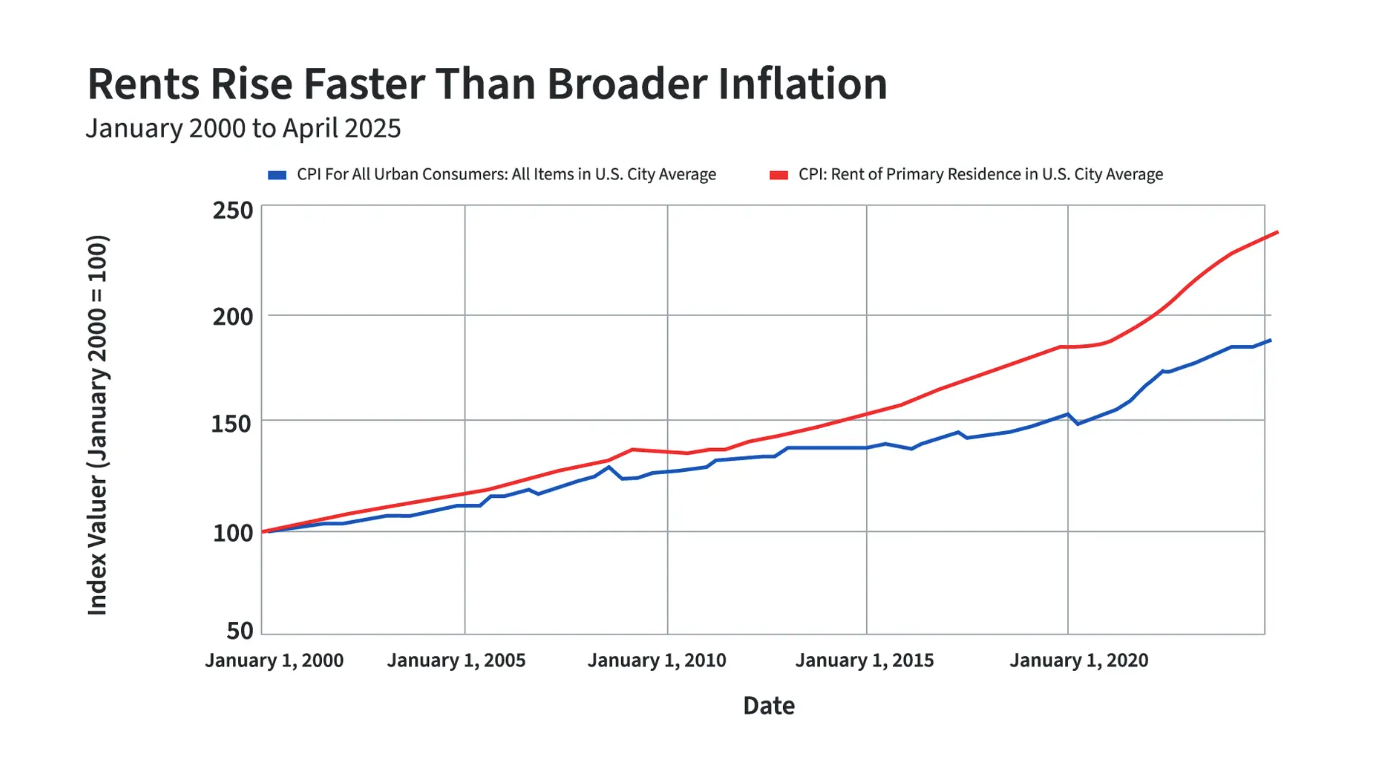

Like private real estate in general, multifamily assets are typically valued using an income-based approach. This means the more income a multifamily community produces, the more it’s worth. Here, what sets multifamily apart is the resilience of the asset subclass’ rental income in the face of inflation.

Specifically, residential rents have outpaced broader inflation by a cumulative 26% since the beginning of the century.5,6 This historical tendency for rents to keep pace with or exceed inflation means that the income generated by multifamily properties rises in tandem with the cost of living.

This, in turn, could potentially drive continual increases in property valuations and serve as a potential hedge against inflation for multifamily investors.

One advantage of investing in multifamily through a private real estate fund, in particular, is that your fund manager can, in certain cases, influence or exert direct control over the underlying deals. When making multifamily equity investments, fund managers can potentially participate in the acquisition, construction, renovation, management, and disposition of assets. These actions can directly impact rents (and thus valuation), offering a pathway to "forced appreciation" not typically available in public markets.

Similarly, multifamily debt fund managers can practice rigorous underwriting, leverage strong lending relationships, and use creative loan structuring techniques. These hands-on approaches, which aim at limiting loan losses and enhancing yields for investors, can potentially result in higher risk-adjusted returns for investors in comparison to the more rigid and standardized public fixed-income markets.

What’s the takeaway?

For high-net-worth investors interested in alternatives to publicly-traded assets, private multifamily real estate funds offer several compelling advantages:

Because multifamily real estate is priced using fundamentals rather than daily market sentiment, it tends to fluctuate less in value. This allows your capital to potentially compound more consistently, without the frequent need to recover from deep losses.

Multifamily real estate behaves differently from stocks and publicly-traded bonds. Adding private multifamily funds to your portfolio can potentially serve as a hedge against inflation and make it more resilient to downturns—especially when public markets struggle, like they did during the 2000s.

Private real estate fund managers can sometimes directly influence the underlying equity or credit investments they make. Skilled managers can potentially protect capital or enhance returns for private real estate investors in a way that is difficult to replicate in the public markets.

These advantages aside, private real estate funds can also potentially help you unlock unique advantages* not available to stock market investors, including depreciation, 1031 exchanges, or payment priority in the form of preferred returns. This unique risk profile, coupled with an ability to counterbalance public market swings, could make private real estate a compelling alternative for high-net-worth investors.

Tired of the stock market rollercoaster? Consider private real estate investment funds from DLP Capital today.

Is investing in property better than the stock market?

There’s not a universally “better” investment; property and stock investments arguably both have a place in your portfolio. However, property investments can potentially serve as a hedge against inflation, generate ongoing cash flow, and deliver capital appreciation over time—all with less annualized volatility than the stock market.

Which is better, equity or real estate?

Neither equities nor real estate is objectively “better,” since they feature differences in liquidity, volatility, and annual returns. That said, real estate as a whole—and private real estate funds in particular—can potentially be less volatile than equities, and may allow investors to benefit from tax advantages (like depreciation or 1031 tax-deferred exchanges) not available to equity investors.

What investment is better than the stock market?

Private real estate could potentially be better than the stock market in delivering more consistent and less volatile returns over time. Unlock stocks, some real estate strategies like private credit can also benefit from an elevated interest rate environment.

Does Warren Buffett invest in real estate?

Yes. Beyond his primary residence in Omaha, Nebraska, which he purchased in 1958 for $31,500 (about $350,000 in 2025), Buffett also owns a 400-acre farm 50 miles north of Omaha, which he purchased from the FDIC for $280,000 in 1986, or about $817,000 in 2025. Buffett’s most significant real estate investment occurred in 2017, when he acquired a 9.8% stake in the publicly-traded REIT STORE Capital for $377 million.

Should I do stocks or real estate?

You don’t have to choose—you can (and should) allocate to both stocks and real estate. A Cornell study, for example, found that real estate should make up about 9% of your portfolio; various other studies have found an allocation of 10–20% to be optimal in terms of diversification. Stocks, bonds, commodities, and cash can comprise the remainder of your portfolio.

Our website uses cookies to enhance your experience, analyze website traffic, and deliver content tailored to your interests. By clicking "Accept", you consent to our use of cookies.